Palm Oil Lorry Crash: Can You Claim Fire Insurance? A palm oil lorry tanker crashed into the front portion of a house, causing severe impact damage to the hall. This house is situated beside a main road. Whom should you claim for impact damage? Such incidents are commonly seen in daily newspapers. What is […]

Month: February 2017

Utmost Good Faith: Insured and Insurer’s Binding Part V

Utmost Good Faith Binding Between Insured And Insurer Part IV Two policies cover the same consignment, a small claim response, but the insurer rejected the bigger sun-insured claim. The story of the insurer not following the Utmost good Faith rule by the insurer. In Malaysia, it is common for the insured or a transporter to […]

Utmost Good Faith: Insured and Insurer Binding Part IV

Utmost Good Faith: Insured and Insurer Binding Part IV. The insurer has a bigger role in Utmost Good Faith binding both parties, namely the insurer and the insured. Liver Transplant Tragedy Friday, June 7, 2002, on Singapore Strait Time, carried the title “Transplant tragedy: Heartbreak for wife: ‘He died not knowing I was pregnant.’ Transplant […]

Utmost Good Faith: Insured-Insurer Binding Part III

Utmost Good Faith: Insured-Insurer Binding Part III. How did the insured make use of the loophole of the Utmost Good Faith? I am eager to prove my capacity to earn the non-motor insurance profit commission besides the normal agent commission during my first year as an agent/broker after I quit my full-time job in a […]

Utmost Good Faith: Insured and Insurer Binding Part II

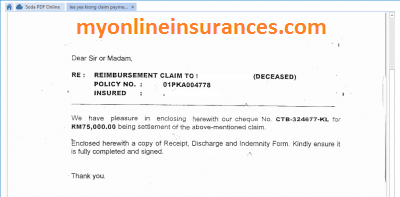

Utmost Good Faith Binding Between Insured and Insurer Part II What is Fraudulent Misrepresentation? Fraudulent misrepresentation, also known as concealment, happens when the insured fails to disclose important information. For an insurance company to deny payment due to concealment, it must prove that: The insured knew the fact was crucial for the insurance being applied […]

Utmost Good Faith in Insurance: an essential principle

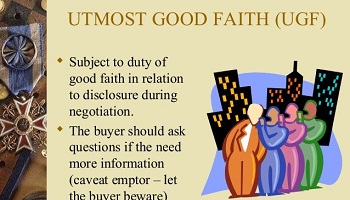

Utmost Good Faith in Insurance: Essential Principle, how it applied to the insurer and insured in the proposal. Utmost good faith, or Uberrimae Fidei, is a key principle in insurance law. It requires everyone involved in an insurance contract to act honestly and disclose all relevant information. The insured must provide accurate details […]

Insurer Denies Claim: Genuine Fire, No Settlement

Why no claim? When I joined a public listed insurer, my branch manager handed me a mountain of claim files. I diligently reviewed them at home, working late into the night. After a month of local training, I attended another two weeks of training at the headquarters with senior underwriting and claims managers. Yet I […]

Banking Secrets: Why Pay More? Part III

Banking Secrets: Why Pay More? Part III What is indemnity? Indemnity means compensation for loss, damage, or injury. It’s a contract where one party agrees to pay for the losses or damages incurred by another. Usually, this stems from a contractual obligation to protect against liability, loss, or damage. Simply put, insurers pay to reinstate […]

Banking Secrets Revealed, Why Pay More? Part II

Banking Secrets Revealed, Why Pay More? Part II. Please refer to my Banking Secrets Revealed, why pay more? Can the ground that erected your house can fire it down? When you buy a landed property, be it freehold or leasehold, the housing developer will charges you the land price too. In Malaysia, it is charged […]

Insurers Idnemnity New for Old Electrical Appliances?

Insurers Indemnity New for Old Electrical Appliances? Can you believe it? If insurers do pay your claim.The public would have two responses.” I….s that tr…….ue? Martin asked with his unbelievable eye. ” Yes, my Led Television which I brought in 2014, the recent lightning damaged it, the insurer paid me the 2017 current price” Mary […]