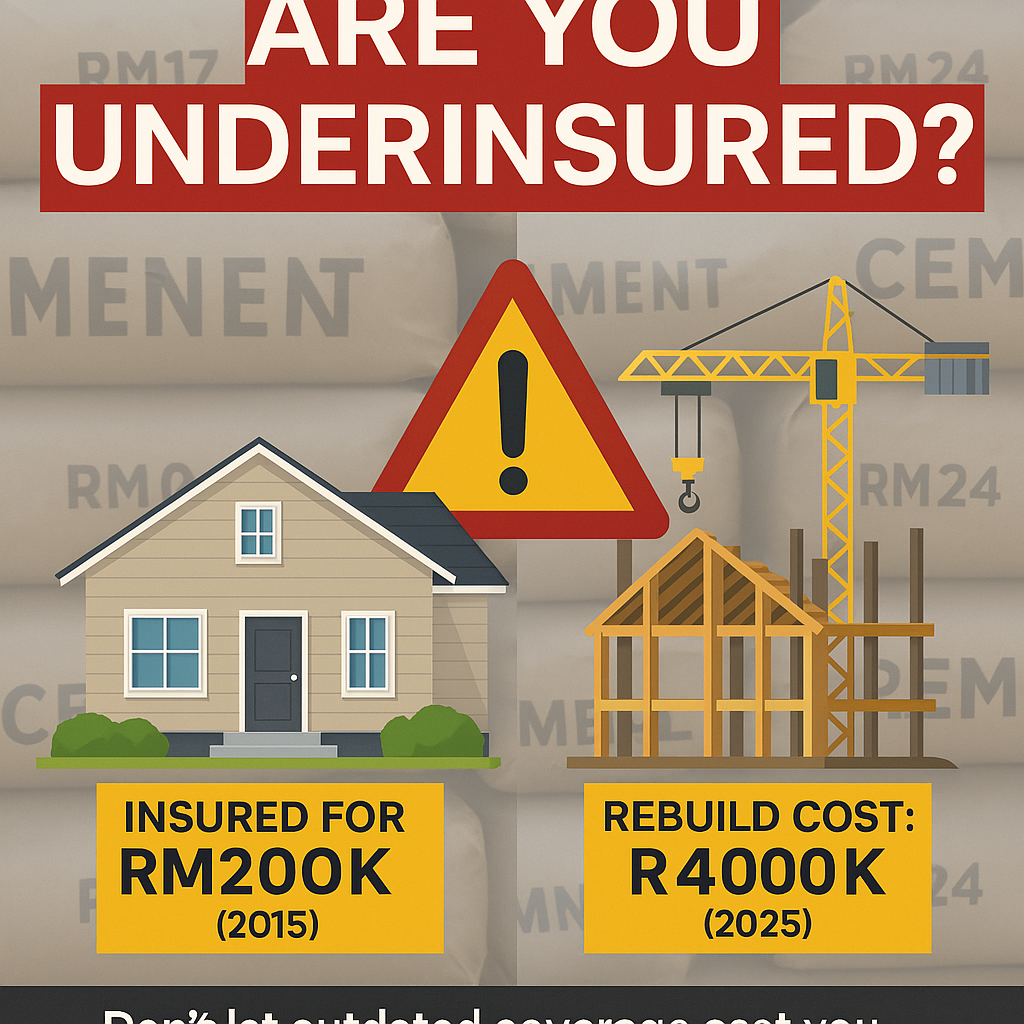

Danger of Underinsured The Hidden Danger of Being Underinsured. How can being underinsured cost you everything? Learn how inflation affects the sum insured and why accurate coverage is critical in a total loss claim. ⚠️ The Hidden Danger of Being Underinsured: What Every Property Owner Must Know Imagine this: your home was insured for RM200,000 […]

Author: jamin

Born in a beautiful valley undulating Kluang town in the heart of Johor, there is 400 plus coffee shop with a population of 300K+. Enjoying high tea with coffee with charcoal toast bread inherited by the British planters.

Generally speaking, people drink coffee to awake the whole night either to burn the midnight oil for a student or for some unfinished task. Conversely, I don’t enjoy coffee.

Is coffee a sleeping pill?

But it is not my cup of tea. Why? If I suffer from insomnia, I would drink coffee, retire to bed, and sleep like a log till the following day. Coffee is a sleeping pill for me. It sounds weird to many, including my family members and my best buddies on the campus.

Sipping black tea to stay awake the whole night, Burning the midnight oil before the examination, never exists in my dictionary.

” Hi, buddy, did you see Jamin around? one of my buddies asked another hotel inmate.

“Why?” my friend asked him.

” I need his help for solving the General Average calculation.”

” He has gone for a movie show just now” he gave my friend a bewildered look.

Peculiar Way

A day before the examination, I hardly do any revision. To reward me for three months of preparation, I instead went to a movie to calm my mind. Stress and tension will lower your score in the examination, my belief.

My Journey

Nevertheless, I joined the shipping department of one of the conglomerate groups of the company under Robert Kuok. To excel in my work, I pursued the Chartered Institute of Transport (UK), majoring in shipping via self-study. An opportunity for me to have a high tea with HRH Princess Anne when she officially declared the opening of the 1st MRT of Singapore in November 1987. HRH gracefully shook hands with all the top experts in the shipping industry from Singapore and Malaysia, including me.

After ten years of seeing the sunrise and never seeing the sunset in the evening jumped out from stressful routine work in the shipping industry and seeded my own logistics company.

Four years down the road, my business is getting more stable. One day, one of my secondary seniors asked me to join Malaysia British Assurance Bhd. It later merged with Allianz General Insurance Company(Malaysia) Bhd to open the marine market for this establishment in 1994.

Hopefully, I acquired more knowledge in general insurance; I enrolled for the AAII, MII, and ACII one after another associate examination by self-study.

Unbelievable, I Passed with flying colors in the examination even though I still operated my logistics company in the morning. It was my term and conditions before being an employee of the insurer.

Thus, I became a boss in the morning, Corporate Marketing personnel in the afternoon, and a self-study student at night. Diligently study for 3.5 years to clear the 19 subjects instead of 4. Wasn’t it a surprise?

Only attend the six-day study conducted by MII on Marine Insurance and Marine Hull one month before the final day. My secret weapon uses the subconscious mind to study while you are sleeping.

Ultimately, I received a gold medal from our ex-central bank of Malaysia governor Tan Sri Dato’ Sri Dr. Zeti Akhtar Aziz for scoring Distinction in the ACII final paper Marine Underwriting and Claim. The only recipient for the graduation ceremony held in Putra Worl Trade Centre in Kuala Lumpur.

The Central Bank of Malaysia gave a Marine Adjuster Licenced to me a year later.

successful Claim grey area

A UK life insurer paid the whole amount of RM32,000. And RM2,700.oo interest incurred for the delay in the settlement. The insured canceled the life policy after 1.5 years.

A composite insurer settled RM75,000.00 on a cashless medical policy. It denied the claim because the insured took the slimming pill from a general practitioner. It is an exclusion clause in the policy.

The insured had two separate policies from the same insurer covering identical products and incidents. A daylight hijacking. A hijacker stole the handphone microchip consignment costing RM900,000.00 in 10 minutes while the box van was parked at the Plus highway resting area. The insured was willing to pay RM250,000.00 for settlement but refused to pay another RM500,000.00 policy. Finally, both approaches responded.

Coaching and Seminar

I worked as a facilitator for the Federation of Malaysian Manufacturers (FMM) for cargo insurance for shipper students. I delivered a speech on How to avoid the subrogation clause with Pan Lorry Owner Association.

Call me/WhatAapps +60 013-7839857

I like to challenge the insurers on the gray area on the claim matter. Keep learning and improving myself by sharing knowledge and coaching others examination candidates. It is my way of contributing back to society.

Fraud and High Medical Claims Cause Premium Hikes

Understanding the Link Between Fraud and Rising Medical Insurance Premiums.The escalating cost of medical insurance premiums is a concern that continues to plague many individuals and families. While several factors contribute to this upward trend, two key elements stand out: fraud and high medical claims. Understanding the link between these two factors and rising medical […]

Excess Claims Drive Health Insurance Premium Hikes

Understanding the Impact of Excess Claims on Health Insurance Premium Hikes Excess Claims Drive Health Insurance Premium Hikes. The escalating cost of health insurance premiums is a concern that continues to plague many individuals and families across the globe. One of the primary drivers of these increases is the prevalence of excess claims. Understanding the […]

The principle of utmost good faith with example

Understanding the Principle of Utmost Good Faith through Real-Life Scenarios The principle of utmost good faith with example , also known as “uberrimae fidei,” is a fundamental tenet in the world of insurance and contract law. It is a legal doctrine that requires all parties involved in a contract to act honestly and not withhold […]

How to claim flood damage to your car?

Steps to Successfully Claiming Flood Damage for Your Car How to claim flood damage to your car? When you find your car submerged in water due to a flood, it can be a distressing experience. However, it’s important to remember that you can claim flood damage for your car from your insurance company. This process […]

Claim flood damage in Malaysian fire insurance

Understanding Flood Damage Coverage in Malaysian Fire Insurance Policies How to claim flood damage insurance? In Malaysia, the interplay between fire insurance and flood damage coverage is a topic of significant importance, particularly given the country’s susceptibility to monsoonal rains and flash floods. Understanding the nuances of how flood damage is addressed within the framework […]

1 principle: utmost good faith binding insured and insurer

1 principle: utmost good faith binding insured and insurer. The principle of utmost good faith, also known as “uberrimae fidei,” requires both the insurer and the insured to act honestly and disclose all relevant information when entering into an insurance contract. Here’s a true-to-life example in the context of general fire insurance: Example: Scenario: John […]

Does Travel Insurance Cover Earthquakes and Tsunami?

Does Travel Insurance Cover Earthquakes and Tsunami? Does Travel Insurance Cover Earthquakes and Tsunami? Travel insurance typically covers a range of risks, including earthquakes and high-altitude sickness. For instance, if an earthquake strikes while you’re travelling, your policy may cover medical expenses, trip cancellation, and emergency evacuation However, it’s crucial to check the specific terms, as some policies exclude coverage for natural disasters in high-risk areas. High-altitude illness Travel insurance often includes medical expenses and emergency evacuation if you fall ill during a […]

Understand tour bus liability and travel insurance

We need to understand tour bus liability and travel insurance. There are vast differences between the types of insurance. Let’s break down the differential between tour bus liability and travel insurance. **Tour Bus Liability:** – **Coverage Scope**: Specifically covers incidents that occur on the tour bus. – **Primary Focus**: Protects the tour company against claims […]

Householders protect homes with peace of mind

Householders protect homes with peace of mind Householders protect homes with peace of mind in today’s world, we should protect our homes with peace of mind by having a householder policy. Safeguarding our homes is more important than ever. Yet, many homeowners overlook the crucial step of getting householder insurance. Recent surveys reveal a startling […]